March 2026 Almond Market Report

California handlers experienced their largest monthly shipment volume since November 2025, up 16.5% over last year per the March Position Report. Right on schedule, domestic shipments saw their first YoY gains in over a year (+1.9%) as monthly shipment volumes have cycled through a rebalancing at a new average shipment volume that began the previous March. Forward volumes to domestic markets are expected to continue to fall in line with this new average volume. Export markets were +21% YoY in March with shipment volume on the crop year growing at a +2.99% pace. Net shipment volumes are off -1.87% on the crop year.

The industry does not typically process much incoming volume in March, but what was processed fell below volumes last year widening the gap between crop receipts ever so slightly from last year to -0.6%. Total supply after accounting for a smaller carry forward is -1.11% below last year.

Total Committed Shipments remains above last year’s figure by +0.43%. March marked another strong purchasing month with over 240 million pounds put on the books. This was a record volume for March and came on the heels of a record setting February.

Water Outlook

As of April 1st, the traditional peak of Sierra Nevada snowpack, California had recorded one of its lowest snow levels on record totaling just 18% statewide of normal volume. The Northern snowpack was even worse at just 6% of normal. The small snowpack was a consequence of warmer winter storms that dropped less snow and particularly warm spring that brought accelerated early season melting.

Rainfall totals in and around California’s growing regions were not as dire with most reporting stations reporting an average of 75-85% of normal. This has helped the Central and Southern growing regions maintain a zero drought designation according to US Drought Monitor. Furthermore, reservoir levels continue to be above historical averages, with many at or above 90% full capacity. This will help alleviate some of the supply pressures that a low snowpack would create as summer runoff will decline earlier than normal; but reservoir levels are expected to hit their peak levels earlier this year with draw down beginning sooner than average. This could put water levels in a deficit to start our next water year next Fall, increasing the risk of drought impacts should precipitation continue to fall below average next season.

Long term forecasts are predicting El Nino conditions to develop in the Pacific. If this persists into the Fall, California could be in store for a wet winter. In fact, some of California’s wettest years have occurred during El Nino years. But even with a persistent El Nino, precipitation can be elusive, while other weather impacts like warmer temperatures and higher humidity could present added stressors to the current growing season.

Export Markets

India imported over 39 million pounds in March improving to a -3% pace on the crop year. India had been behind by as much a -41% YoY when a late harvest and tight carry forward limited what California handlers were able to ship. As supplies rebounded, India has continued to demonstrate its strength as an important driver of demand for California almonds.

Western Europe experienced an especially strong shipment month in March, surpassing volumes from a year ago by nearly +43% as a region. On the crop year, regional markets are up +6% on net. A year ago, Spain was experiencing significant declines and was off -18% on the crop year. A year later, Spain has rebounded fully and has even surpassed volumes seen at its peak two years ago. The Netherlands has basically experienced the inverse seeing a return to previous volumes a year after experiencing significant growth. Elsewhere in the region, Italy maintains its newfound title as the second largest regional importer of almonds up +15% on the crop year, with Germany not too far behind up +6% for the crop year.

The Middle East imported -8.3% fewer almonds in March than it did a year ago. Considering war in the region, this could be read as a rather resilient figure. Quite predictably the UAE saw a near cessation of shipment volume with the blockage of transit through the Strait of Hormuz, but Turkey, being less impacted by the conflict, nearly doubled its volume from a year ago and is now up +30% on the crop year. Saudi Arabia also saw modest growth YoY in March and may be called upon as a trans-shipment market to supply UAE traders if logistics disruptions in the Strait persist. On net the region’s pace of growth slipped a bit after disruptions in March, but remains on the positive side at +4% for the crop year.

China and Southeast Asian

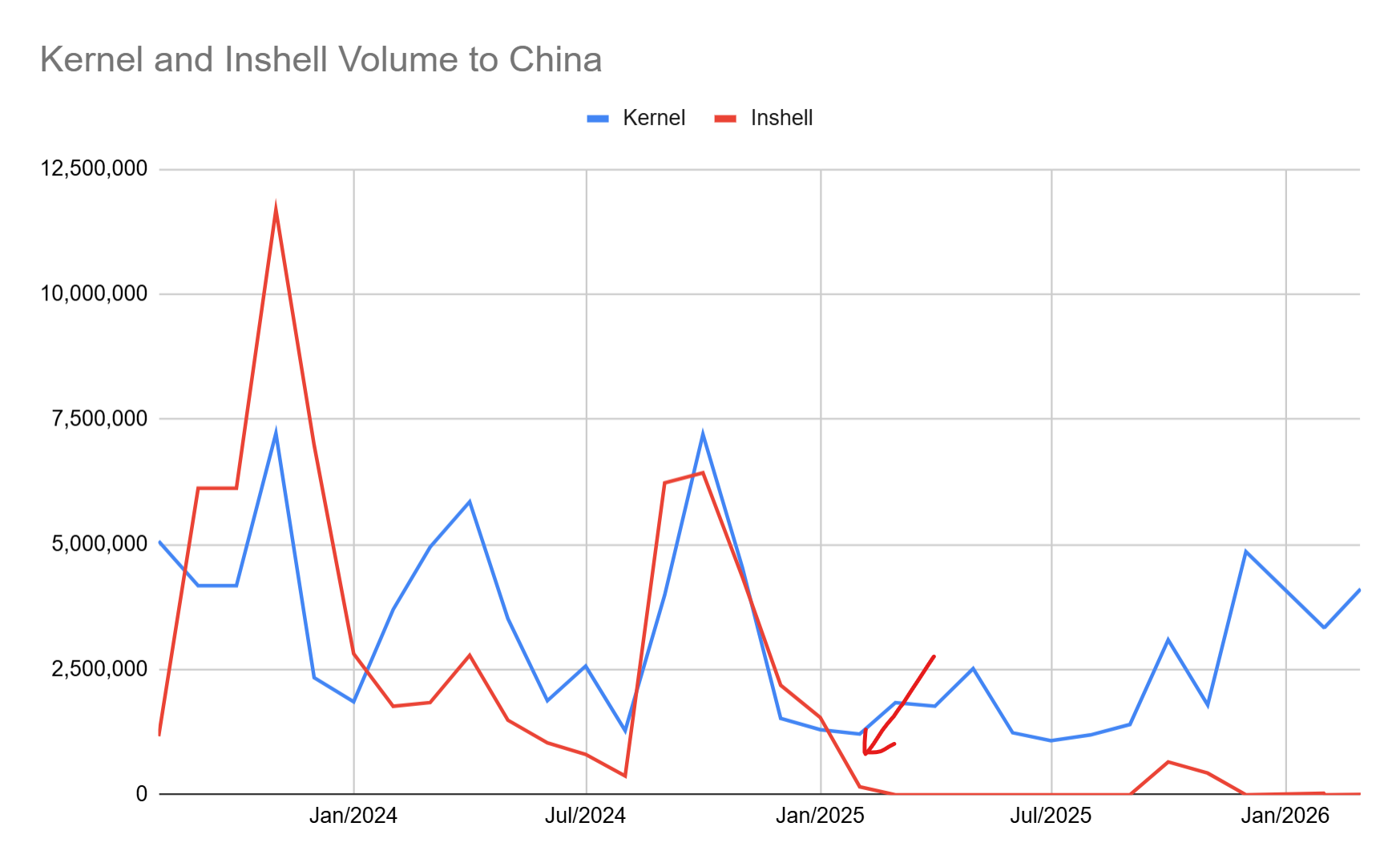

We have long observed that shipment volumes to China have been on the decline, and we have seen volume to value-added markets in Southeast Asia increase in response. But it is important to understand that the shipment declines directly into China observed this crop year have been driven in large part by an effective collapse of inshell shipments. In fact, for the crop year, kernel shipments into China are actually up, albeit modestly at +1.1%. Inshell shipments on the other hand are off -94.7% on the crop year. This trend can be traced back to Feb/March of 2025 when the US and China first traded tariffs at the beginning of President Trump’s second term.

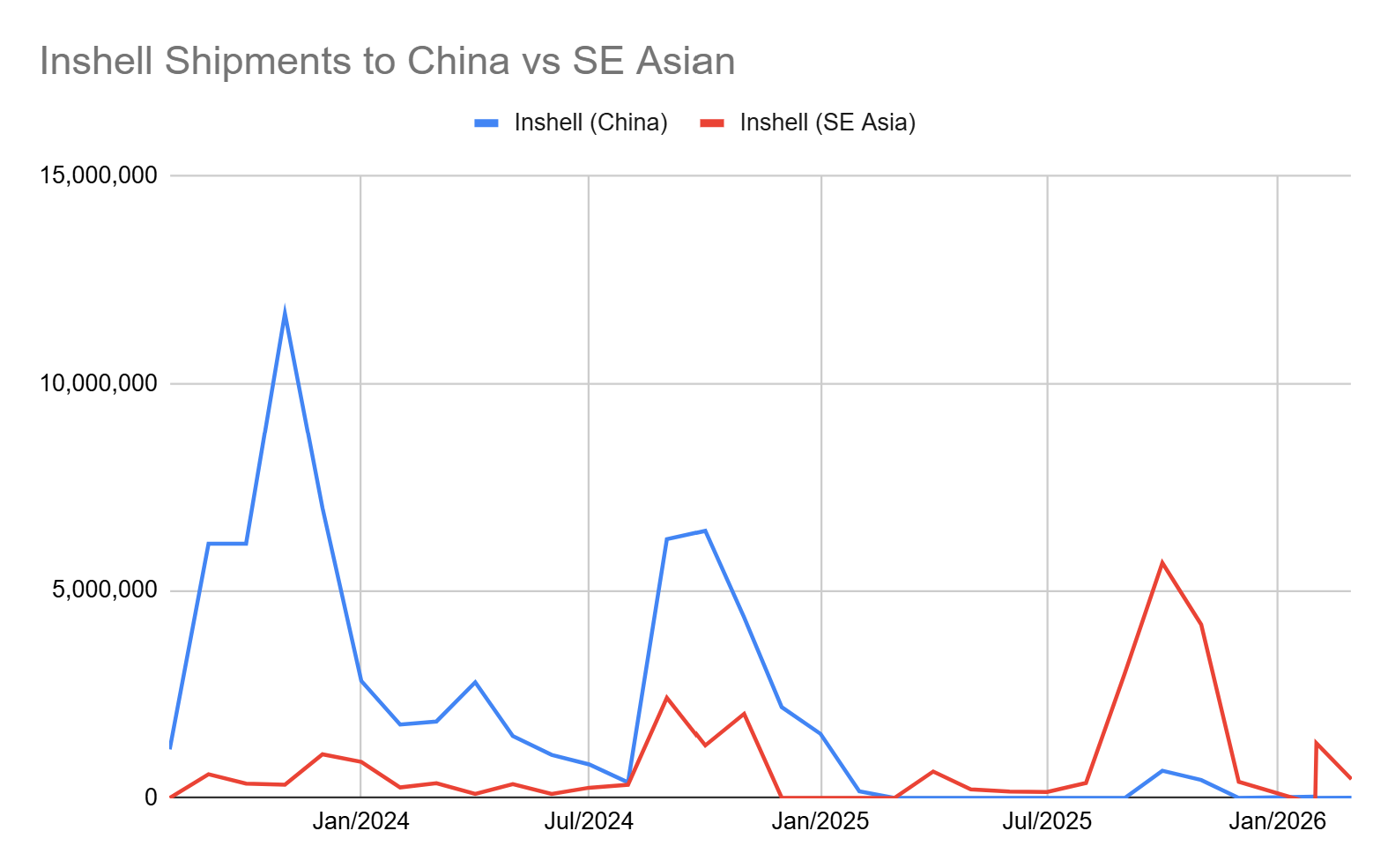

As we have seen Southeast Asian markets grow to provide value added services for the almond supply chain into China, the question concerning inshell shipments is whether the lost volume is simply being re-routed through these growing SE Asia markets. The following chart plots inshell shipment volumes to China and the SE Asia region over the past two plus crop years:

What the chart suggests is that during peak demand cycles in China, SE Asian markets may very well be servicing the needs of Chinese buyers for inshell product. But shipment volumes drastically taper off outside of this peak demand season implying the Chinese buyers are leveraging other sources, like Australia, when supply needs are more modest.

The longer term trend for kernel shipments directly into China has been down, but it’s encouraging that shipments on average have remained stable when inshell volumes fell. Recent kernel shipments have been on an upward trajectory, outpacing monthly volumes from a year ago for four straight months. We will be watching to see if this trend continues, or if markets were experiencing a more protracted rebalancing like the peak observed in Oct/2024. At the very least the kernel volume highlights the limitations of shifting supply chains and capabilities of value-added and supplemental markets when it comes to satisfying Chinese demand for almonds.

Shipments into Southeast Asia continue to be strong with most markets seeing sizable growth on the crop year. Vietnam is up +63% and has accounted for the majority of the volume growth in the region. But other markets like Thailand (+22), Malaysia (+45%) and Indonesia (+43%) continue to develop their markets and are experiencing significant growth as well.

Global Supply

Australia’s production of almonds has been steadily growing over the past several years. While production remains well behind California, Australian almonds have become a viable supply buoy to global markets. For instance, China has found Australia to be a valuable alternative in the face of tariffs on US goods, and India has come to rely on Australia for quality inshell product when high end inshell supplies tighten as California heads towards its seasonal transition.

What was originally forecast as another record harvest for Australian growers has now come under questions with significant weather events impacting harvest. Sustained wet weather is already having having impacts and growers in the region are seeing decreased quality in their inshell products. While the overall volume is not expected to be overly impacted, markets looking for high quality specifications and inshell products from Australia are going to find less available inventory, increasing pressure on supplies from California.

In our previous section examining shipments into China and SE Asia, we see inshell shipment volumes increasing in February and March, implying we may already be seeing the impacts of tightening inshell supply from Australia. It's entirely reasonable to expect more inshell volume into SE Asia in the months ahead helping to bolster shipments of California almonds into the region and putting further strain on inshell supplies from California.

Market Analysis

The current state of the almond market certainly leans bullish. California handlers effectively have the same on-hand inventory as a year ago at this time meaning handlers would need to ship about 209 million pounds a month for the duration of the crop year to target the same carry forward as a year ago. But supply and demand will be better balanced if the industry targets a carry forward figure closer to 525 million pounds, implying shipment volume averaging 200 million pounds per month would be an acceptable figure.

Handlers may also be reluctant to sell too much into a smaller carry forward with questions about the current crop lingering. Bloom conditions were not ideal. Well above average temperatures this spring have many concerned about an extreme summer. Growers have also faced soaring input costs raising concerns about long term orchard health. We are still waiting for official forecasts to help form expectations on eventual crop size, but consensus has clearly built that California is not expecting a large supply increase come harvest, meaning handlers are likely to be cautious, at least until more clarity is at hand.

Shipment figures and purchasing have continued to be strong demonstrating global demand for California almonds. The largely global hand-to-mouth buying pattern is going to continue to put pressure on the industry to maintain strong shipment figures, but the torrid pace of purchasing is likely to return back to normal levels. This could create periods of balance in the market, but the transition approaches preferred specifications and new prompt shipment contracts are going to face added pressures. If shipment volumes in April remain elevated these pressures are only going to be exasperated.