June 2026 Almond Market Update

As expected, little changed on the supply side of the equation in the June Position Report with crop receipts effectively steady from a month ago and off -0.73% YoY. Total supply, after factoring in the carry forward and loss and exempt estimate of -2%, is -1.21% behind last year. It should be noted however that in both the current year and previous year the inedible rate ran higher than the -2% historical average and is current -2.63% with very little additional receipts expected. This would reduce the current calculated computed inventory down under 680 million pounds. This is an important consideration when historically the industry has found supply and demand in balance at a 20% stock-to-use ratio, which at current shipment levels, would fall roughly within a range between 500 and 550 million pounds. At current inventory levels, a modest shipment volume of 180 million pounds in July would put the industry at the bottom of that target volume and shipments in excess of 180 million pounds could put additional supply side pressures on the industry.

Shipments in June neared 213 million pounds, up +14.1% over last year. For the crop year, shipment volumes on net are off just -0.95%. Export shipments on the crop year are up +3.06%, while domestic shipments are off -12.74%, though as we had noted in past reports, domestic shipment volumes have stabilized around 50 million pounds per month indicating that domestic purchasers have found a balanced buying pattern.

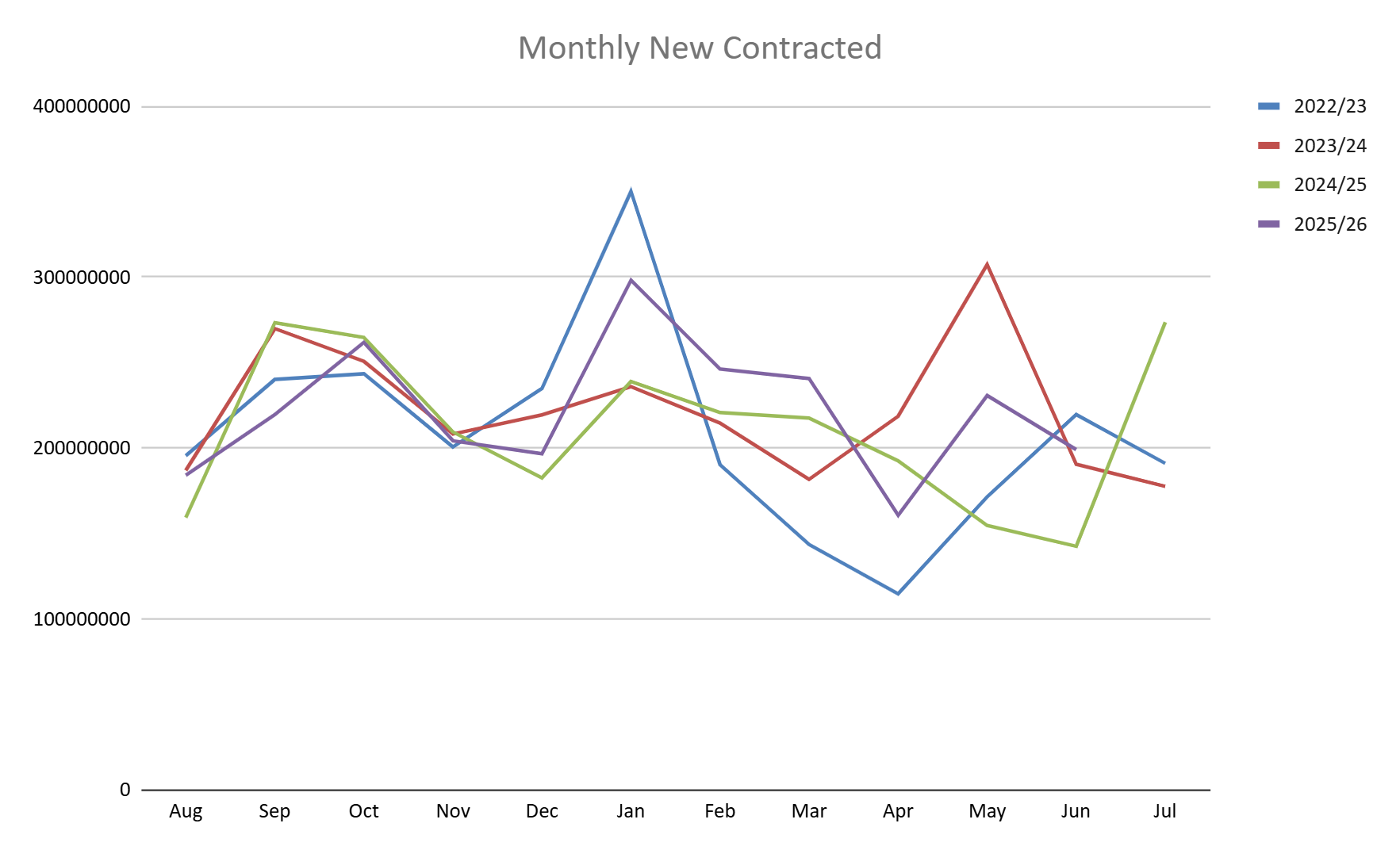

The position report notes that total committed shipments is up +17.96% YoY with uncommitted inventory down -17.79%. While these figures illustrate that monthly purchasing activity has been more accelerated than a year ago, taking a longer term view will show that monthly purchasing has generally fallen in line with recent historical trends. For instance, June purchasing volume neared 200 million pounds, up almost +40% YoY, but when looking at other recent years this volume falls between levels for the 2023/24 and 2022/23 crop years. In charting purchasing volume of recent years, not only can we see that current volumes do not fall into extremes, but we can also see that last July saw a significant up tick in contracted volume that we will almost certainly not see this year. This simply reflects the caution and uncertainty that the industry faced last year during the spring that doesn’t exist in the same manner this year. The take away is that current market conditions have allowed for healthy and active purchasing as we head into the transition.

Export Market Review

Imports of kernel almonds to mainland China/Hong Kong are up +9.1% YoY. But this figure hardly tells the story of shipment volumes to China. Inshell shipments have almost come to a complete stand still pushing net volume across all varieties down -35% for the crop year. Furthermore, kernel volume is about half of what it was before tariff and trade disputes ratcheted up in early 2025, and net shipment volumes are down further still from volume levels seen before trade disputes materialized in 2018. While some year over year growth in kernels is welcome, it is clear that California will not be a direct supplier for all of China’s almond demand so long as trade restrictions exist, and likely for some time thereafter.

While we might not have a full view of Chinese almond demand, we can still gain inferences about its needs by taking a larger region view. Markets with value-add capacity in Southeast Asia continue to see strong growth. Though shipment levels were down regionally for June, shipment volumes for the crop year have still paced +27% growth with Vietnam up +29%, Thailand up +8%, Malaysia up +33%, Singapore up +53%, and Indonesia up +36% as the region’s largest markets (listed largest to smallest by volume to date). Growth has been observed in both kernel and in hell volumes, with inshell imports more than doubling from a year ago.

India imported over 34 million pounds of almonds in June, effectively matching volume imported a year ago. Imports for the crop year however are off -9%, more or less ensuring that India will end the crop year (which ends July 31st) down YoY. The shipment volume in June though was a strong demand signal in the face of tightening supply and generally rising inshell prices coupled with recent volatility concerning the Rupee to US Dollar exchange reality. Looking ahead, Indian buyers will be looking to get in front of Diwali demands and are likely to be active through the transition and into early crop receipts as supply allows. This should keep upward pressure on early season inshell shipments. Because 2027 Diwali falls earlier in the season, the upcoming 2026/27 crop is going to need to supply two festive cycles, effectively guaranteeing stronger demand over the entirety of the new crop year and raising the risk of strong supply pressures a year from now.

In our previous Market Report, we touched on the significant volume growth that Pakistan has seen this year. Again in June, we see this trend continuing with Pakistan experiencing a +296% growth rate on the crop year having imported over 28 million pounds. It should be reiterated however that we are not attributing this growth to consumption growth, though there may well be on the ground consumption increases. Instead, the volume increases we are seeing in the Position Report are resulting from shifting supply chains with normal trade channels through trading partners in the UAE having been significantly disrupted. What we’re interested in watching is whether any of this supply chain shifting sticks once supply chains through the UAE normalize. If Pakistani buyers find operational efficiencies in directly importing from California they may be reluctant to return to the trading market as fully as they had. This could free up additional capacity for traders based in the UAE to seek new markets helping to further global demand growth. There are of course plenty of assumptions baked into that simplification, but changing supply chain functions can indeed open up additional opportunities and identifying where those might be manifesting will be something that we will continue to monitor.

Western European markets were collectively up +12.75% over last June’s shipment figure and are up +4% for the crop year. Spain, as the largest regional market, is up +18% YoY on the crop year, topping 182 million pounds. In 2023/24 Spain imported 173.9 million pounds through June down slightly from 178.8 million pounds in 2022/23. This suggests that the YoY growth is Spain returning to its historical norm, rather than a broad growth trend. It should be noted however that local orchard production capacity has grown over recent years, so a return to historical shipment volumes could very well indicate some level of consumption growth on the ground.

Elsewhere in Western Europe, Italy continues to hold an edge in its claim as the second largest market in the region topping 98 million pounds on a +6% growth rate on the crop year. The Netherlands are unlikely to recover the nearly 6 million pound deficit behind Italy for the number 2 ranking, but recent monthly shipment volumes have come more in line with those from a year ago and helped reverse the downward growth trend that now stands at -23% for the crop year. Germany is up +4% on the crop year and has topped 90 million pounds and could still vie to overtake the Netherlands for the number three spot before the crop year ends. Rounding out the current top five markets is the UK with a more modest 32 million pound shipment volume for the crop year, but a +7% growth rate YoY. Don’t discount Belgium though who has earned the 6th place title for the moment with 30 million pounds on an impressive +79% growth rate.

In the Middle East, the UAE was able to handle a significant import volume in June bringing in 10.5 million pounds, up +27.6% from a year ago. Local pipelines are likely going to continue to be constrained as long as active conflict persists regionally, but shipments making it to port is a welcome sign. As it stands the UAE is down -24% on the crop year with significant trading volume shifting to Turkey in the face of regional conflict. Turkey, for its part, is up +42% on the crop year and continued to see significant growth in shipment volumes YoY in June with volumes up +41.8%. Elsewhere in the region, Saudi Arabia almost tripled its shipment volume YoY in June. Shipment volumes for the crop year are still down -15% however. Israel is up +99% for the crop year topping 16 million pounds and could be a source of additional growth regionally in the coming crop year.

Forecast - Or Lack Thereof

Traditionally July brings the Objective Forecast, but the USDA recently decided to forego this exercise, so the Industry enters the summer without this forecast benchmark for the first time in quite a while. This is arguably the biggest wildcard the industry has. There have been several industry players to recently develop forecasting models who have subsequently widely shared their forecasts publicly, but even so, we now lack a neutral forecast mechanism with transparent methodology to at least balance industry sentiment against.

The reality though is that sentiment has always been a strong driver even with an Objective Forecast in place. This is simply because a relatively small fluctuation in supply can have significant impacts in markets and industry forecasts have long been misunderstood. Consider the 2025 Objective Forecast whose headline figure called for 3.0 billion pounds. Receipts per the May Position Report totaled 2.69 billion pounds. Was the Forecast accurate when it overestimated yield by 310 million pounds?

The answer I suppose depends on your perspective, but statistically speaking, the 2.69 billion pounds fell in line with the statistical model as noted in the fine print: “The 80% confidence interval is from 2,610 to 3,390 billion meat pounds”. Practically speaking 310 million pounds can significantly move markets. So ask yourself this instead: If the Objective Forecast instead of reporting the midpoint published a 2.61 – 3.39 billion pound range would it be given as much weight in the market? The answer of course is no, that range is too broad to make any meaningful assumptions on, but this is the reality of what the Industry has been operating under. Consequently sentiment, grower reports, earlier field returns, and huller receipts have been much more important signals in directing markets. This hasn’t changed.

Does that mean the Industry wouldn’t continue to benefit from a neutral forecast as an additional waypoint to balance sentiment and reporting that is largely in the hands of the suppliers? Perhaps not, but be careful not to overstate the value of a tool that wasn’t what many purported, or wanted it to be.

So where does that leave us? The Industry still seems to be largely coalesced around a 2.7 billion pound figure, but recent forecasts and reporting shared publicly has started to soften expectations around this figure. Our own observations and communications from our grower community supports the notion where a 2.7 billion pound target persists, but where we assess more risk in yields falling short of this figure than exceeding it.

Market Review

Almond commodity prices have largely been on an upward trajectory post bloom and generally speaking markets have continued to purchase. As the industry looks ahead into the transition and beyond into next year, the supply side of the equation looks to continue to tighten. The carry forward could easily fall below 500 million pounds and signal tight inventories as harvest begins. With a forecast of 2.7 billion pounds that many are beginning to feel will come in a bit lighter, the industry is essentially looking at a scenario where supplies at best are able to sustain current shipment levels through the next crop year.

As prices inch upward with sustained upward pressure, it is reasonable to question if the more cautious hand-to-mouth buying patterns we seen this year, especially from India, may be signaling markets nearing the edge of price acceptability. This is a fundamental question of any market. As we read it, we see a market that has been generally balanced but is coming to terms with converging bullish pressures. Export markets have shown continued growth as prices have inched higher and many remain poised for additional growth; and, production costs have continued to suppress orchard plantings and bearing acres are beginning to decline weakening the long term supply forecast as fewer trees mature and orchard removal accelerates. With domestic demand seemingly finding a new normal a 2.7 billion pounds forecasted for next year presents a no growth environment, which will inevitably pit emerging growth markets, price sensitive ones, and developed markets against one another. As evidence of this, our sales teams has reported growing interest in longer term contracts as those with the economic capacity to do so are beginning to gain confidence in long term price trajectories.

For now, as long as supply levels don’t come in significantly below target, price fluctuations are likely to be modest, but longer term trends over the course of the crop year are likely to point upward. Consider a scenario where post bloom next year we have a forecast that continues to show incremental declines in expected yield and have India looking for supplies out of the current crop for the second Diwali season of the crop year. It’s much easier to imagine a scenario where prices have risen than retreated. Don't be surprised when next year's annual price charts continue to show an upward trend.